Derivatives 101 Part 4: Swaps Contracts: Total Return Swaps and Archegos Capital Management

Derivatives 101 Part 4: Swaps Contracts: Total Return Swaps and Archegos Capital Management

This is the final part of the derivatives series (for now). So far, we’ve covered forwards, options, and futures. This morning, we’re going to cover the final major derivative — swaps.

Remember, a derivative, in a nutshell, is a pricing guarantee. The common elements of derivatives are:

There is a buyer and there is a seller.

Value is derived from the underlier.

There is a future price.

There is a future (exercise) date.

To make swaps accessible, let’s frame the concept around a simple example.

A company — let’s call it the Artificial Intelligence Monolith (AIM) — has borrowed $30 million dollars (i.e., the notional, or principal amount) from a commercial bank, the Valley Intelligence Bank Entity (VIBE). Under the terms of the loan (i.e., every three months for the next two years), the AIM will make an interest-only payment based on a floating rate of interest according to the Secured Overnight Financing Rate (SOFR) index. AIM, today, doesn’t know how much interest it will pay for this loan.

Of course, AIM will aim to reduce its exposure to changing interest rates. Therefore, AIM enters into a fixed-floating swap agreement with Montgomery Securities (MS). Under the terms of the swap (i.e., every three months), AIM will make an interest-only payment on $30 million to MS based on a fixed rate of 5.25 percent. In return, AIM will receive from MS an interest-based payment based on SOFR: AIM will use this to make its payment to its bank, VIBE. Using the swap, AIM has effectively converted its floating-rate obligation to a fixed rate and mitigated its exposure to unpredictable interest rates.

In this example, as the “seller of money” at a fixed price of 5.25 percent, Montgomery has the short position. Likewise, AIM has the long position, as it’s buying at that rate. Ultimately, as we can intuit, a swap is simply an exchange of cash flows. Remember, borrowing money typically requires paying interest at regular cadences over the life of that loan, just like a once-a-month payment for a mortgage. Each of these interest-rate payments is a cash flow, with the cash “flowing” from the borrower to the lender.

The Mechanics of Swaps

In practice, the mechanics of swaps is a bit different:

One party is nearly always a big investment bank (specifically, its prime-brokerage division) or a derivatives dealer. It’s usually not another debtor with an actual obligation.

Often, the principal amortizes over the life of the contract, so interest payments may compound or be based on an average rate.

Swap counterparties will typically execute a master agreement before working out particular swap (underlier) trades. A master agreement details the terms that apply to any trade that two parties might execute.

A master agreement almost always includes a set of International Swaps and Derivatives Association (ISDA) definitions, which exactingly prescribe what’s meant by specific terms and schedules (i.e., actual/360).

For most swaps, the notional (or principal) amount — the number used when it comes time to calculate payments — is often just a computational convenience and isn’t actually necessary to change hands between counterparties.

However, in currency swaps, folks (counterparties) need to be cognizant of FX rates as exchange rates will inevitably fluctuate and cause one party or the other to “pay a price” because of the changing value of the other’s currency. Therefore, by exchanging notionals at both ends of the trade, counterparties mitigate risk by effectively removing the exchange-rate uncertainty from the picture; as you can intuit, the purpose of an interest-rate swap is to remove interest-rate uncertainty.

Credit Derivatives

There are many flavors of swaps within credit derivatives. Credit derivatives — namely, the three most common credit derivatives: credit default swaps (CDS), total return swaps (TRS), and credit-linked notes (CLN) — deal with the counterparty credit risk associated with that party fulfilling its financial obligation.

In other words, remember how derivatives are basically pricing guarantees — well, you can think of credit derivatives as variations of performance guarantees as you’re effectively dealing with the non-zero chance your counterparty fails to fulfill its financial obligation.

The incentives behind utilizing such a financial instrument are straightforward: essentially, a credit derivative like a total return swap (which will be covered shortly) enables unbundling your overall risk into individual components of risk, each of which can be addressed on its own for whichever specific (risk) use case. For instance, a fixed-floating swap can hedge away your exposure to changing interest rates. Atop that, a credit default swap can be added into the mix to hedge away your exposure to counterparty default risk.

Total Return Swaps and Archegos

Now that we have an understanding of credit derivatives, let’s dive into total return swaps. The incentive for using a total return swap is straightforward: essentially, a TRS enables entities like a hedge fund to enjoy (or suffer) the economic consequences of owning an asset (e.g., equity, etc.) without actually owning it. In other words, the accounting terminology would be “off its balance sheet” as the hedge fund would essentially be “renting” the asset from the bank’s balance sheet for the duration of the contract.

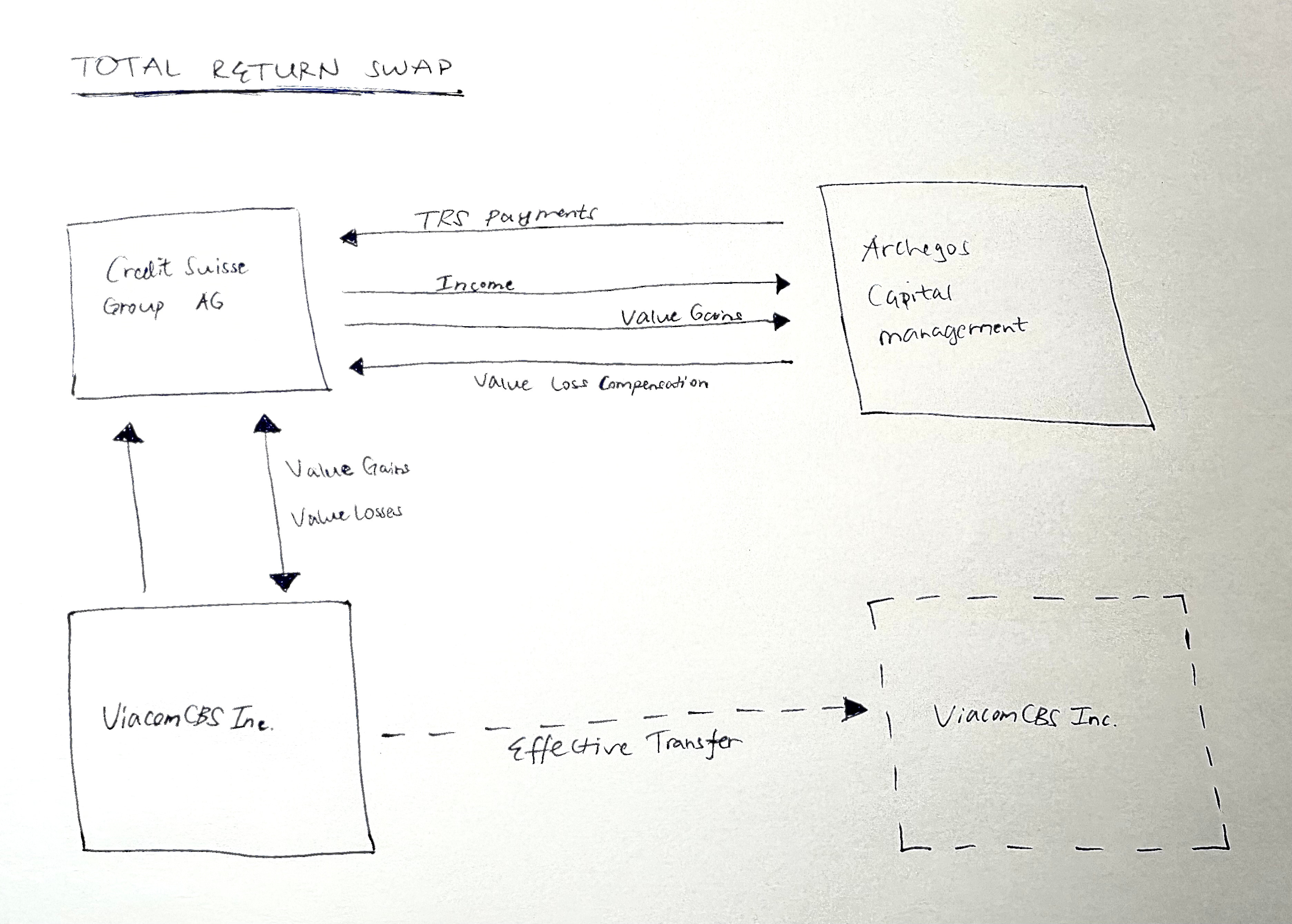

To put this into perspective, the following diagram’s framework shows the different participants and cash flows in a real-life total return swap example that eventually led to the blow up of Archegos Capital Management and the subsequent market-manipulation lawsuits against its founder, Bill Hwang, that ensued not long after; those lawsuits are actively being heard at trial today.

The participants of this TRS are:

The protection buyer is Credit Suisse Group AG.

The protection seller is Archegos Capital Management.

The asset that’s being effectively transferred (or “rented”) from Credit Suisse’s balance sheet is a plain equity, ViacomCBS Inc.

The mechanics of this TRS are:

Archegos (the protection seller) makes a stream of regular payments — let’s imagine SOFR plus 50 bps — to Credit Suisse (the protection buyer).

In exchange for those payments, Credit Suisse (the protection buyer) transfers to Archegos (the seller) all the income a la coupon payments and capital changes (e.g., changes in market valuation) with respect to a reference asset — in this case, the “total” return of the single-name equity, ViacomCBS Inc. — but Credit Suisse continues owning the equity for accounting purposes.

The bidirectional payments are generally lined up to “swap” at the same time.

Archegos (the seller) compensates Credit Suisse (the buyer) for value loss due to any reason, not just credit events.

Now, here’s the simplified version of the Archegos story:

“Archegos Capital Management was a family office run by Bill Hwang, a former Tiger Cub hedge fund manager, that invested his personal fortune. Starting in about 2020, Archegos’s investment strategy consisted of buying a whole ton of shares of like 10 stocks, using mostly money borrowed from about a dozen banks. (Technically it did this using total return swaps rather than actually buying the stocks on margin, but that is a minor point.)

As Archegos kept buying more of these stocks, they went up, because generally if you buy a lot of a stock the price will go up. As the prices went up, Archegos had mark-to-market profits: The shares it bought earlier at lower prices were worth more, so it had made money. Archegos used these profits, leveraged with more money borrowed from its banks, to buy more of its favorite stocks. This made the prices go up more, which created more profits, which gave it more money to buy more stocks, etc., in what I guess you could call a virtuous cycle.

. . .

There was a small hiccup with one of its stocks: ViacomCBS Inc., a huge Archegos holding, saw its stock price shoot up and decided to raise some money by selling stock, which pushed down the price a bit. The result was that Archegos was absolutely vaporized almost immediately: It got their margin calls that it couldn’t meet, its stocks were liquidated, their prices crashed, it lost all its money, and some of its less nimble banks lost billions of dollars when they were too slow to liquidate. It is the obvious outcome and it happened.”

The two sets of regulations underlying this series of events are Regulation T and Schedule 13D. Regulation T of the Federal Reserve Board mandates that Archegos can only borrow up to 50 percent of the purchase price of securities that can be purchased on margin; having purchased securities — like ViacomCBS Inc. and Discovery Inc. — on margin would have required Archegos to abide by that 2:1 ratio. Basically, if Archegos wanted to buy $5 billion in ViacomCBS stock, it would first need to own $2.5 billion of ViacomCBS stock outright to buy the other $2.5 billion. Archegos circumvented these leverage rules by entering into total return swaps with banks like Credit Suisse Group AG, making Credit Suisse the actual owner of the stock. Of course, Archegos would bear the risk of loss should the price of the stock fall. Similarly, Archegos would reap the benefits if the stock went up. TRSs at many different big investment banks’ primes ultimately enabled Archegos to buy massive amounts of stock without having initial margin requirements, so Archegos was heavily leveraged. Banks are rational players, and once Viacom took a slight hit, banks one by one (like how a prisoner’s dilemma plays out) realized they needed to sell their positions to protect themselves, which then spurred further sell-offs until Archegos could no longer cover all the value-loss compensations across all their agreements. This leads to the second set of regulations — Schedule 13D and, by extension, Schedule 13F of the Securities Exchange Act — emphasizes transparency and disclosure requirements that would have helped detect Archegos’ market activities. A Schedule 13D filing to the SEC is required once an investor acquires — directly or indirectly — 5% of a voting class of stock. A Schedule 13F filing to the SEC is required to track the investment discretion of investments over $100 million that are traded on a national exchange. Archegos basically circumvented these two devices by leveraging total return swap contracts and its titular status as a family office — this status made Archegos exempt from registering with the SEC under the Advisors Act. Consequently, Archegos had no 13D or 13F disclosure and transparency requirements to fulfill.

Now, here’s the more detailed version of the story — Bloomberg Businessweek synthesized the details well:

“The first in a cascade of events during the week of March 22 came shortly after the 4 p.m. close of trading that Monday in New York. ViacomCBS, struggling to keep up with Apple TV, Disney+, Home Box Office, and Netflix, announced a $3 billion sale of stock and convertible debt. The company’s shares, propelled by Hwang’s buying, had tripled in four months. Raising money to invest in streaming made sense. Or so it seemed in the ViacomCBS C-suite.

Instead, the stock tanked 9% on Tuesday and 23% on Wednesday. Hwang’s bets suddenly went haywire, jeopardizing his swap agreements. A few bankers pleaded with him to sell shares; he would take losses and survive, they reasoned, avoiding a default. Hwang refused, according to people with knowledge of those discussions, the long-ago lesson from Robertson evidently forgotten.

That Thursday, his prime brokers held a series of emergency meetings. Hwang, say people with swaps experience, likely had borrowed roughly $85 million for every $20 million, investing $100 and setting aside $5 to post margin as needed. But the massive portfolio had cratered so quickly that its losses blew through that small buffer as well as his capital.

The dilemma for Hwang’s lenders was obvious. If the stocks in his swap accounts rebounded, everyone would be fine. But if even one bank flinched and started selling, they’d all be exposed to plummeting prices. Credit Suisse wanted to wait.

Late that afternoon, without a word to its fellow lenders, Morgan Stanley made a preemptive move. The firm quietly unloaded $5 billion of its Archegos holdings at a discount, mainly to a group of hedge funds. On Friday morning, well before the 9:30 a.m. New York open, Goldman started liquidating $6.6 billion in blocks of Baidu, Tencent Music Entertainment Group, and Vipshop. It soon followed with $3.9 billion of ViacomCBS, Discovery, Farfetch, Iqiyi, and GSX Techedu.

When the smoke finally cleared, Goldman, Deutsche Bank AG, Morgan Stanley, and Wells Fargo had escaped the Archegos fire sale unscathed. There’s no question they moved faster to sell. It’s also possible they had extended less leverage or demanded more margin. As of now, Credit Suisse and Nomura appear to have sustained the greatest damage. Mitsubishi UFJ Financial Group Inc., another prime broker, has disclosed $300 million in likely losses.”

There is a nice little prisoner’s dilemma that played out in the end among the different prime brokerages. Matt Levine sums up the confusion that you (and I) (likely) have about the underlying rationale about all this:

“But I don’t really understand it, because it is so obvious. Bill Hwang is not some dope; he is a long-time hedge fund manager with a Tiger Management pedigree. The story I laid out above is stupid, and it inevitably ends the way I described. Bill Hwang presumably did not want to lose all his money. What was his exit plan? How did he think the story would end?”